As long time Bitcoiners, we are not shocked by the ongoing confusion around the nature of the bitcoin market. The reality is that, unlike other public markets, the bitcoin market has significantly more noise. There is noise around price valuation, noise around use cases, noise around data and noise from skeptics. It is very difficult for a new person to enter into the bitcoin market and cut directly to the signal.

This confusion has been manifested once again in a misguided article circulating the web: “The Bit Short: Inside Crypto’s Doomsday Machine.”

It seems that the author of the now-viral Medium article has, like many others, slipped into some pretty big newbie pitfalls around bitcoin exchange data, bitcoin’s nature as black market money and, of course, fear, uncertainty and doubt (FUD) around a prominent grey market dollar solution called tether. This article will examine the author’s key arguments one by one and explain these pitfalls, demonstrating why they should not be taken seriously in anyone’s consideration of tether or its relationship to bitcoin.

The root of the tether conspiracy is a fundamental assumption that the bitcoin market is not legitimate and that there is no legitimate demand for bitcoin, only FOMO that is created as a side product of “fraudulent tether printing.” In 2016 or 2017, the tether conspiracy theory was a very powerful narrative. That’s right, these very tether fears existed before 2020… this story is old.

In 2021 in a world where we know fiat is being devalued at an enormous clip, people and institutions are flooding into anything that is not fiat and big wig investors are appearing on TV, discussing their massive allocations to bitcoin. Today, the no legitimate demand story is a lot weaker. Bitcoin is the world’s hardest and scarcest asset created for this express purpose.

While on the surface, “The Bit Short: Inside Crypto’s Doomsday Machine” seems to raise some very credible concerns around the bitcoin market, these concerns are effectively based on misinterpretations of data visualizations that are themselves based on fake data.

Unfortunately, “The Bit Short” is unfounded FUD.

The author is parroting several baised and discredited individuals who have clung to this tether narrative for over four years now.

We do not intend to defend Tether, iFinex, Bitfinex or any other private organization related to tether, we have not spoken to them and they can and do speak for themselves. Rather, we are here to debunk the faulty information in “The Bit Short,” as well as to provide some context so that new investors can avoid the obvious misconceptions that fuel this and many other poorly-researched FUD articles that will continue to propagate.

A Brief History Of Tether And USD-Pegged Tokens

Tether is the original “stablecoin,” which launched in 2014, close to four years before any of its competitors. It is actually tether’s massive success and obvious demand in 2017 that became the impetus for “regulated alternatives” like USDC, GUSD and Paxos to launch.

October 2014: Tether (USDT) Origin Date

December 2017: Dai Stablecoin Origin Date

September 2018: USDC Origin Date

September 2018: GUSD Origin Date

September 2018: Paxos Origin Date

Tether is the biggest stablecoin by both market cap and usage because it was the first. It literally created the stablecoin market and had significant network effects years before any other player started competing. This is not to say it does not have faults, this is just to explain why it is so much larger than its much younger competitors.

Again, this article is not here to defend what tether claims, but rather to help others better understand what tether is and the role it plays. Tether is a black box and is “sketchy” by design. The tether product is for working around the banking system. From a regulatory perspective, this is sketchy by nature. This is also why people use it. Tether users do not want to have their value in the legacy compliant system. The main use case for tether is to sell your bitcoin into a “dollar” without hitting the banking system. In practice, tether resembles future bitcoin buying demand. For many, the point of tether is to circumvent regulations while trading bitcoin.

Raising the alarm to tether’s sketchiness is akin to jumping into the ocean and raising the alarm that there are fish swimming. Of course tether is not outwardly “compliant and transparent,” that is the point of tether.

But the author of “The Bit Short” would have you believe that tether is not only “sketchy,” aka, it serves the grey dollar market, but that there is no bitcoin demand outside of the “sketchy” tether manipulation. We are not arguing that tether is not sketchy, but rather that tether fits in a very nuanced place in the greater Bitcoin ecosystem. We will show with strong evidence that tether does not resemble a fundamental issue in the Bitcoin investment thesis or the legitimacy of the bitcoin market. The author of “The Bit Short” builds their argument on the following points:

- Tether accounts for more than $10 billion in daily inflows to bitcoin

- Tether accounts for over 70 percent of bitcoin trading volume

- Tether issuance must be fraudulent because of how it is issued

- Bitcoin insiders are blind to how tether is manipulating the bitcoin market

- Legitimate exchanges are not affiliated with tether

- Legal authorities are the only way to fix the above issues

While the author’s case makes for a juicy read, especially for readers with little or no understanding of the bitcoin market, upon some observation it becomes pretty clear that these points are based on the misinterpretations of faulty data and general ignorance.

Debunking Point One: “Tether Accounts For More Than $10 Billion In Inflows To Bitcoin”

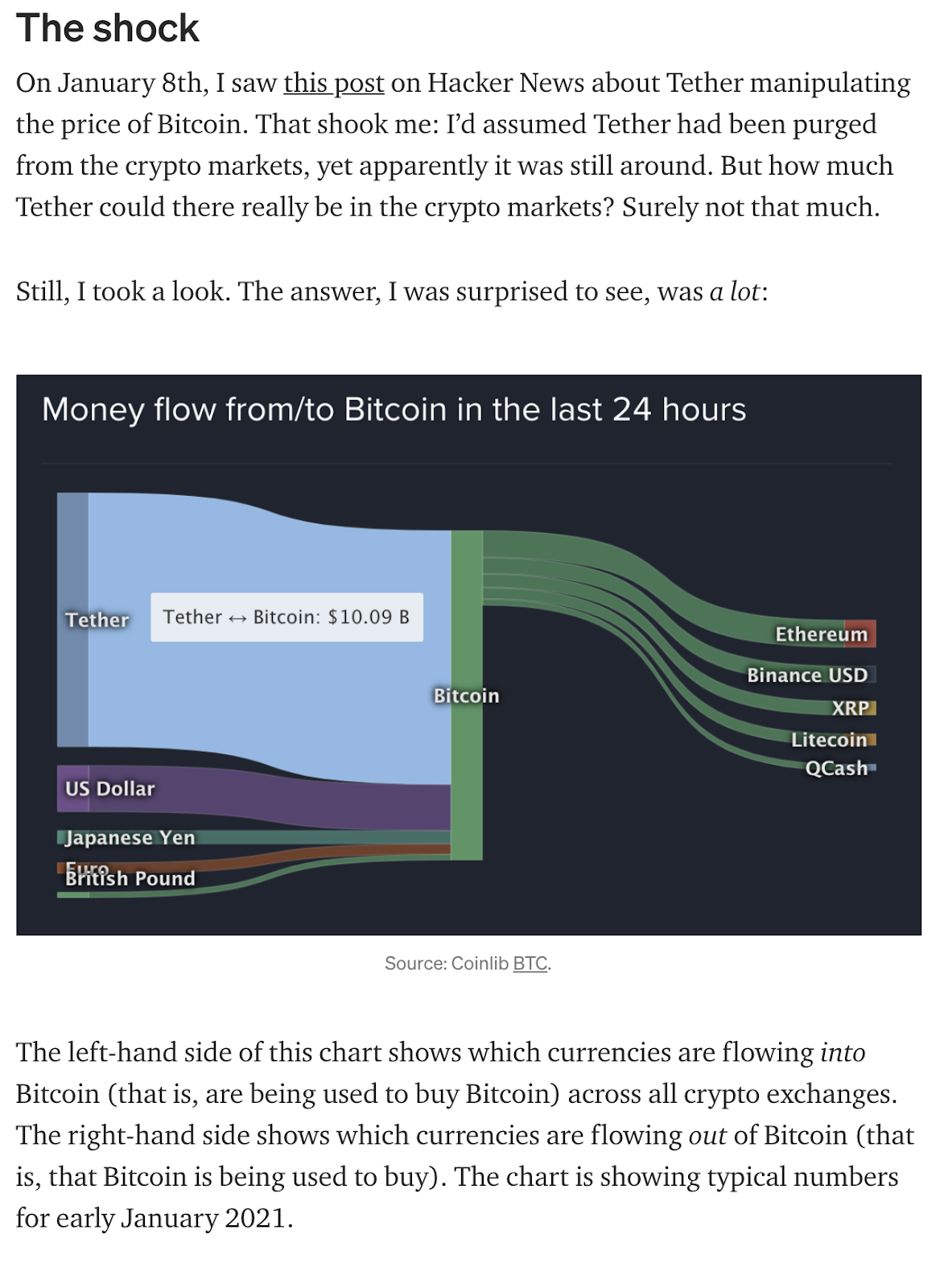

The number-one most important thing about his article is the first chart it displays in the section named “The Shock.”

The author took a screenshot from coinlib.io‘s 24-hour money flow (representing the money that flowed from/to bitcoin in the last 24 hours) and claimed that this chart illustrates one-way buying from tether to bitcoin.

As noted by the data source, this does not represent not one-way inflows, it represents volume. Volume is very different from one-way Inflows. It appears that the author is confused on how to read the graphic they are citing. The author claimed that the left side of the chart illustrates value inflows going into bitcoin and the right side shows values flows leaving bitcoin. This is a completely incorrect interpretation of the chart.

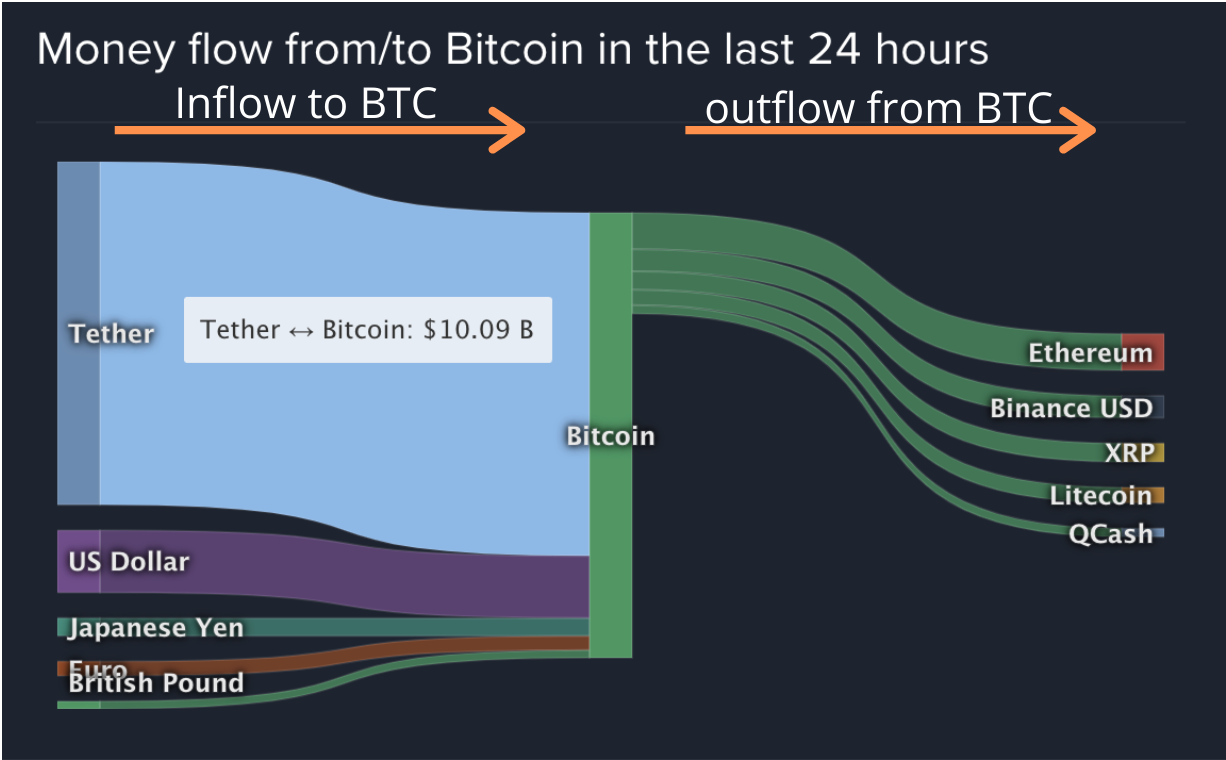

Here is what the author is suggesting the graphic means:

But here is actually what the chart means:

Trading volume does not equal dollar inflows into a system. This is a fact.

With this clear misrepresentation, the foundation of the author’s argument has already completely unraveled due to the fact that tether does not account for $10 billion in inflows on a daily basis. Rather, there is about $10 billion in exchange-reported trading volume of tether.

In the article, the author willingly or unwillingly misrepresented how to interpret the data from these coinlib.io graphics. We will leave it to reader to determine what they believe to be the most likely intent of the author in this misrepresentation.

Debunking Point Two: “70 Percent Of Bitcoin Volume Is Tether”

Next, the author claims that Tether makes up 70 percent of bitcoin’s trading volume.

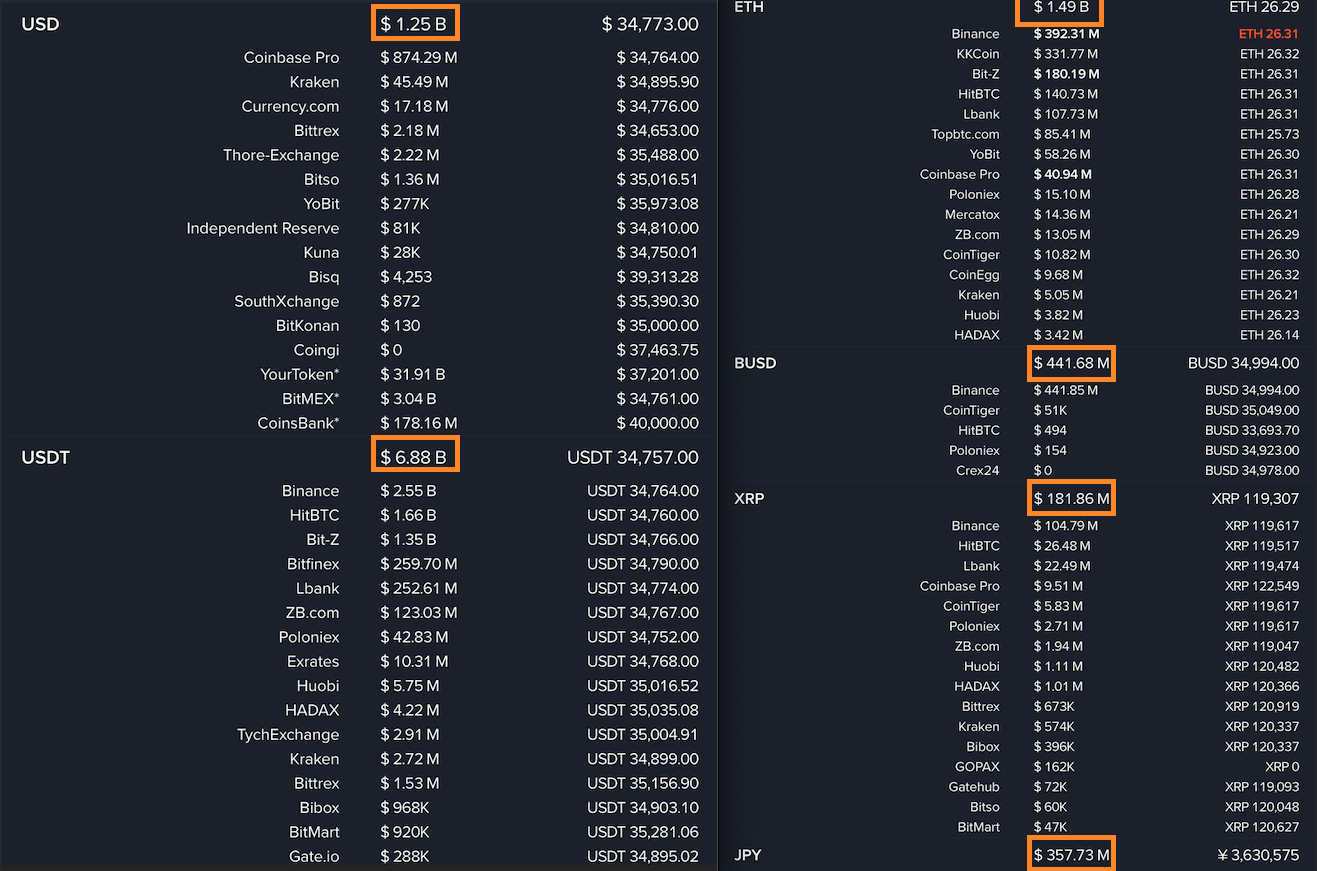

Seventy percent is an interesting figure. How did the author come up with this “fact”? Conveniently, if a coinlib.io user scrolled down from the money flow from/to bitcoin in the last 24 hours graphic, they would find coinlib.io’s bitcoin volume charts.

Also conveniently, if one adds up the total bitcoin 24-hour volume reported on coinlib.io and divides it by the 24-hour tether volume, they would find that about 66 percent of bitcoin trading volume is tether. Here is our math from January 20, 2021, when we conducted this initial investigation:

BTC/USD volume: 1.25 billion

BTC/USDT volume: 6.88 billion

BTC/ETH volume: 1.49 billion

BTC/BUSD volume: 0.44 billion

BTC/JPY volume: 0.36 billion

Total BTC volume: About 10.42 billion

So, 6.88 billion in USDT volume divided by 10.42 billion in total BTC volume equals about 66 percent.

It could be a coincidence that our numbers match up with the “closer to 70 percent” number that the author has claimed, however, we were unable to recreate this exact sum USDT total by percentage of BTC volume from any other resource. Coinmetrics.io, coingeck.com and coinmarketcap.com are all very well-known aggregators which we used to try and recreate the author’s 70 percent stat.

Unfortunately for the author’s thesis, coinlib.io does not have the strongest reputation as a data resource and many exchanges — especially the ones noted by the author — are known to report fake trading volume in order to get free marketing on crypto data aggregators like coinlib.io. The author seems to take coinlib.io’s volume information at face value, when it is in fact almost completely fake.

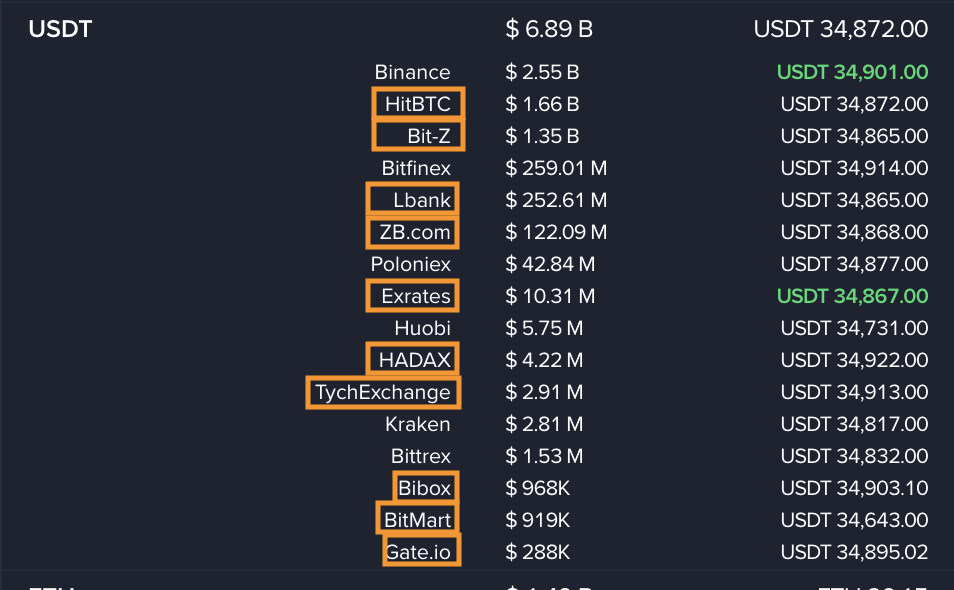

Breaking Down Bitcoin’s Volume In Tether

Let’s further break down the tether volume numbers that coinlib.io highlights:

Coinlib.io shows 6.89 billion in 24-hour tether volume (on January 20, 2021), however not all of the exchanges it used to report that number are legitimate. In fact. most of them are not! We took the liberty of highlighting in orange all of the exchanges that are widely known to participate in fake trading in order to manipulate their rankings on sites like coinlib.io, coinmarketcap.com and coingecko.com.

The author seemed to think that HitBTC and Bit-Z facilitate more real bitcoin demand than Coinbase.

Bit-Z and HitBTC are not large exchanges at all and not even close to two of the biggest. HitBTC in particular has a long history of this kind of unethical behavior. Even Binance, the number-one exchange for tether volume, is known to conduct some shady practices on its exchange to pump up its volume numbers. The main point being that the massive tether volume is not real and absolutely does not represent close to 70 percent of the total bitcoin trading volume. The real trading volume is actually far less than what any of these sites are reporting.

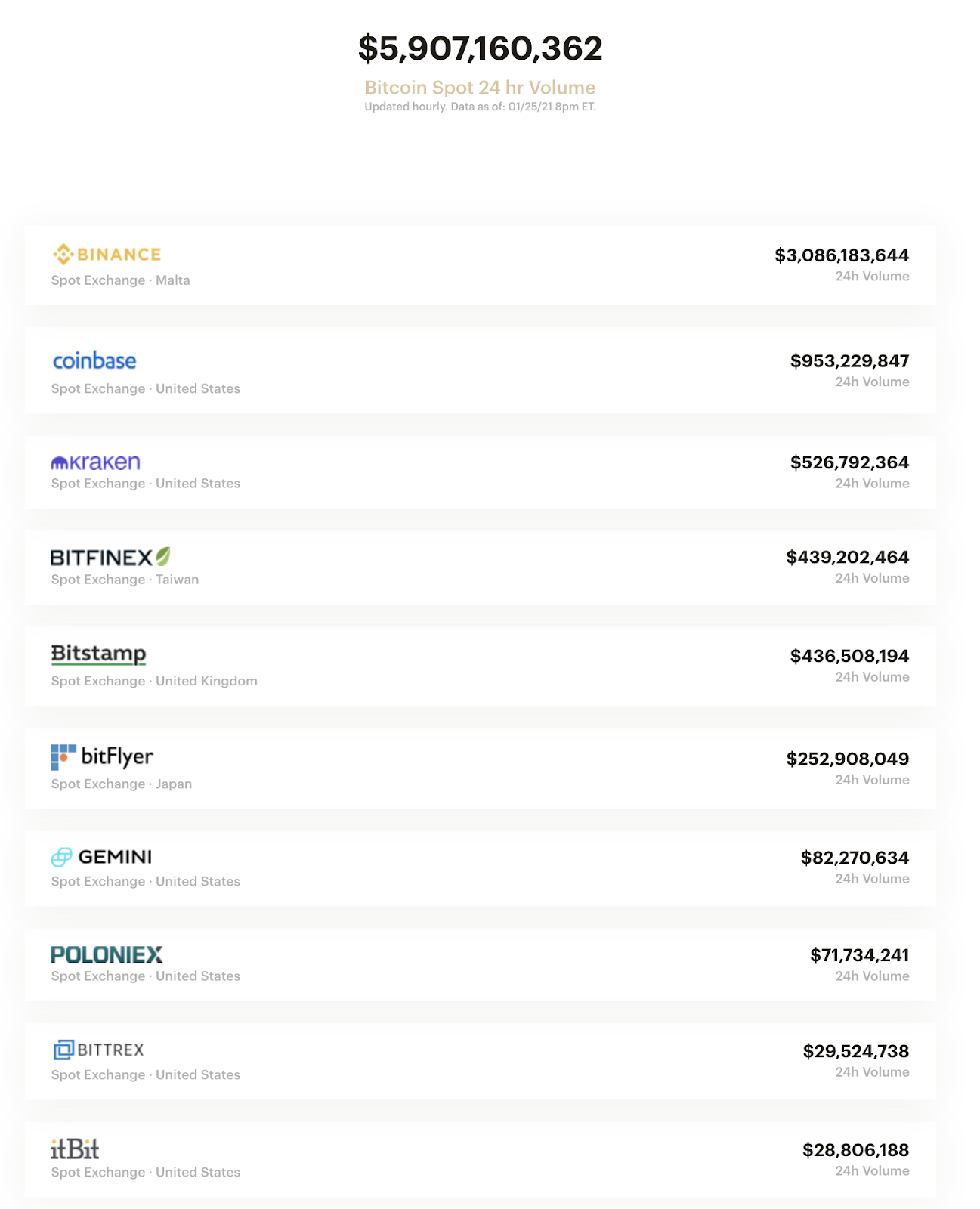

U.S.-based Bitwise did a groundbreaking study in 2018 that showed that 95 percent of bitcoin reported volume is fake! It maintains a website that is designed to give a much better picture of legitimate bitcoin volume.

Bitcointradevolume.com paints a very different picture than those of coinlib.io or the author of “The Bit Short.”

On January 25, 2021, bitcointradevolume.com showed about $6 billion in 24-hour trading volume for bitcoin and just over $4 billion in bitcoin futures volume. It turns out that legitimate bitcoin 24 hour volume is around $10 billion, with over 75 percent of real volume coming from U.S. regulated entities.

At this point, it should be quite clear that the dramatized story that the author of “The Bit Short” has painted is far from reality. Their claims that tether is 70 percent of bitcoin’s legitimate trading volume is far from reality — at most, it represents between 25 percent to 35 percent of real bitcoin trading volume in a given 24-hour period.

Debunking Point Three: “Tether Issuance Must Be Fraudulent Because Of How It Is Issued”

Tether Limited, the organization behind the oldest stablecoin, only issues new tokens to partners. It makes sense that large OTC trading desks receive tether and use tether in large blocks. This is discussed in detail in this excellent podcast with Dan Matuszewski of CMS Holding and Nic Carter of Castle Island Ventures back in 2019.

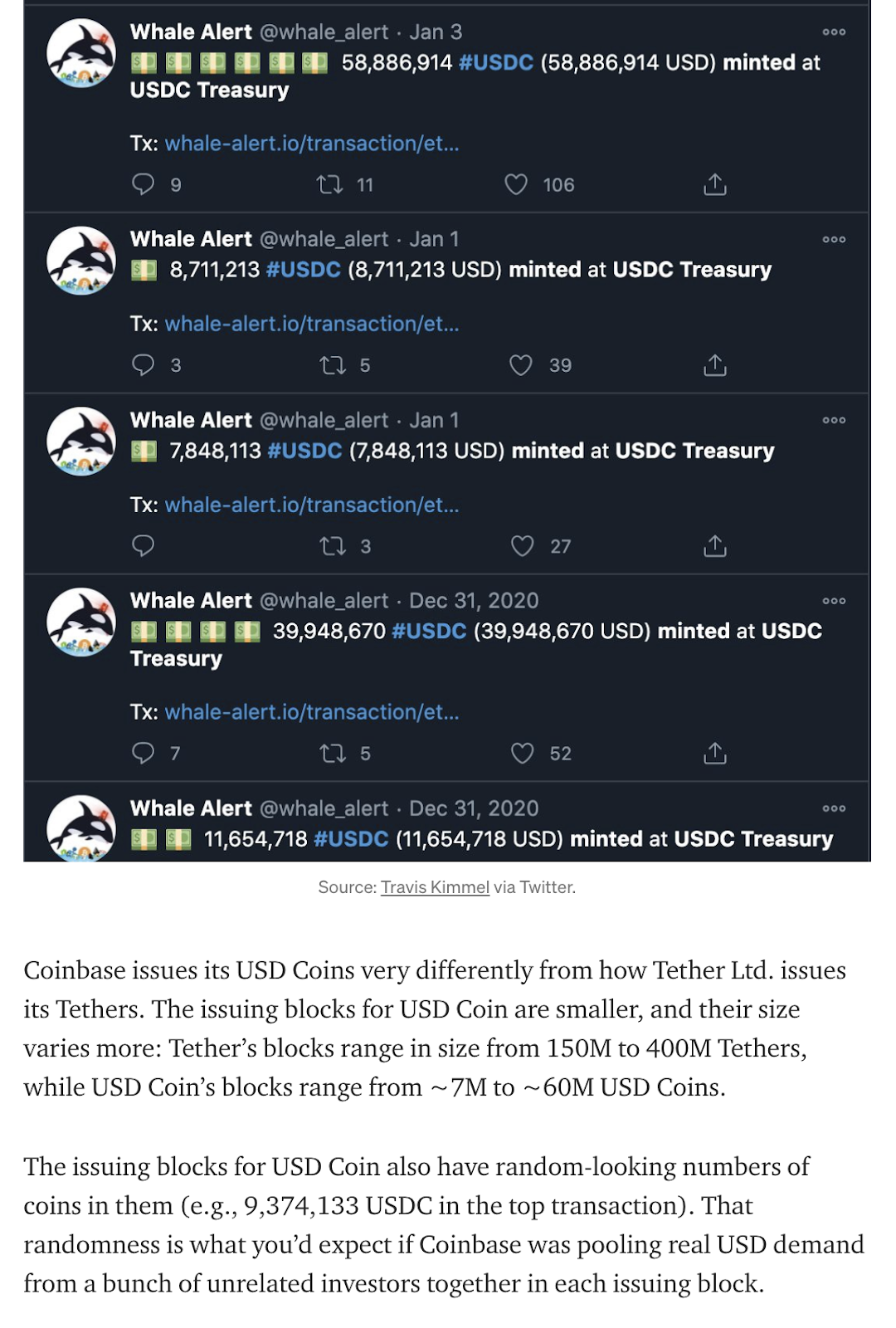

Paulo Arduino, the CTO of Tether Limited, explained the different business models used by Coinbase/Circle and Tether in issuing stablecoins in this 2019 podcast.

USDC from Coinbase has a different model than Tether Limited. Anyone can create a Coinbase account, deposit dollars and mint USDC. If you take a more zoomed out look at total stablecoin printing across the different players, there are actually huge amounts of correlation across all coins.

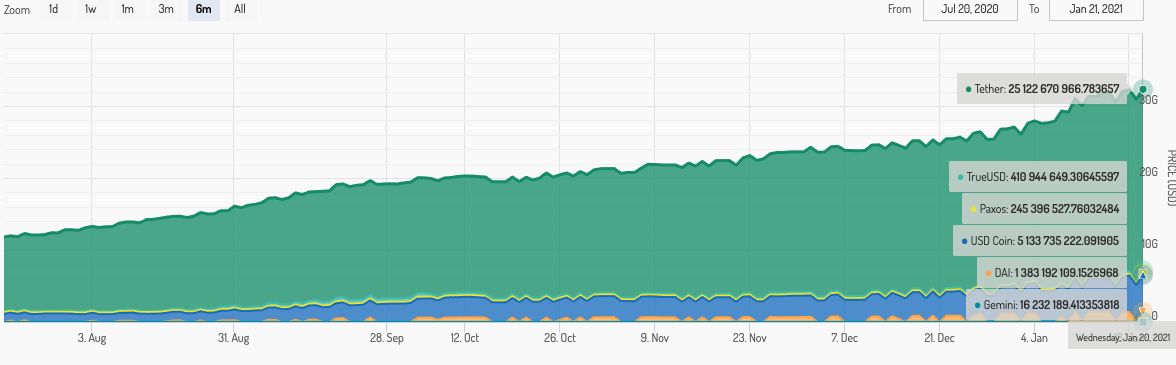

The author asserts that tether printing must be 100 percent fraudulent based on this operational difference between how Tether Limited issues USDT and how Coinbase/Circle issue USDC. We ask the author: Why is stablecoin market cap growth so correlated together? If you look at stablecoin market cap growth across all stablecoins on sites like stablecoinindex.com, it is clear to see that they are growing in sync.

Are all of the stablecoin issuers conspiring and coordinating to print at the exact same time? We seriously doubt that. This distribution of stablecoin market cap growth across all of the players indicates that funds flowing into Tether are likely legitimate and in sync with the rest of the market.

Again, Tether Limited is a black box and we cannot say for certain how it manages its business, but to date, the market has treated tether as being worth $1 consistently.

Debunking Point 4: Bitcoin Insiders Are Blind To How Tether Is Manipulating The Bitcoin Market

We think that, at this point, it is clear that Bitcoiners understand the Tether market far better than the author of “The Bit Short” does. We will just provide a few more examples of Bitcoiners addressing these tired Tether concerns over the years.

2021:

2020:

2019:

LOL! @CNBC’s Facebook page shared a 2 month old Tether FUD article as if it was fresh news. They posted in the afternoon yesterday. I guess they needed some more clicks before year end.

pic.twitter.com/cxOlGvIFZX

— Samson Mow (@Excellion) December 22, 2019

2018:

Debunking Point 5: Legitimate Exchanges Are Not Affiliated With Tether

Bitwise, which offers the Bitwise Bitcoin Fund in U.S. public markets, maintains the aforementioned resource bitcointradevolume.com. On the site, it only lists legitimate bitcoin markets with estimates of what it believes to be legitimate volume.

The following exchanges all offer tether markets and appear on Bitwise’s list; Binance, Bitfinex, Kraken, Poloniex and Bittrex. Five out of 10 legitimate exchanges, according to Bitwise, use USDT. Again, this is another sign that tether is a part of the legitimate bitcoin market.

The most compliant and largest bitcoin P2P market, Paxful, added tether support in 2020 and is based and operated in the U.S. The only two cryptocurrencies it supports are BTC and USDT.

Debunking Point 6: Legal Authorities Are Needed To Regulate Bitcoin

It has become completely obvious to the average investor that the current financial system is rigged against the little guy. This week, everyone from Donald Trump Jr. to Alexandria Ocasio-Ortez has been raising calls against the censorship from apps like Robinhood, WeBull, TD Ameritrade, and the Nasdaq itself. Yet these systems are legal…

Yea I don’t recall the part of the story when Robin Hood sells out and starts to be a mercenary for the crown…

Apparently everyone has a price. #ToTheMoon #GameStop

https://t.co/WPeItjQi9q

— Donald Trump Jr. (@DonaldJTrumpJr) January 28, 2021

We would argue that this final point is the ultimate tell that the author of “The Bit Short” does not understand bitcoin from first principles. Early bitcoin investor Tyler Winklevoss synthesized Bitcoin’s value proposition quite nicely in this famous quote:

“We have elected to put our money and faith in a mathematical framework that is free of politics and human error.”

The famous Latin phrase vires in numeris, “strength in numbers” in English, is another great way to understand the Bitcoin world view. Bitcoin was never about authority, it was always about opt-in, permissionless systems enabled by math and cryptography. For the people, by the people, the people’s money. To call for regulation means that you do not understand the Bitcoin paradigm shift.

One could argue that without the legal authorities’ war on cash, incessant need to tax, dystopian financial surveillance and arcane banking system, there would be no need for tether… if legal authorities are so adept at bringing transparency and integrity to our monetary systems, why don’t they fix their own currency first?

However, there’s a greater point to be distilled here. Bitcoin already is regulated, not by the law of man but by the law of nature. With no “buyer of last resort,” there is nobody to bail investors out from their bad choices… burn me once, shame on you, burn me twice, shame on me. If tether is a scam, it’ll eventually blow itself up. Investors will learn something new, the markets will temporarily go haywire and bitcoin will continue to clear transactions as if nothing ever happened.

Throughout Bitcoin’s 12-year history, it has survived Silk Road, Mt. Gox, OneCoin and much more.

Technical research contributions to this article were made by David Bailey.

The post Debunking Misconceptions From “The Bit Short: Inside Crypto’s Doomsday Machine” appeared first on Bitcoin Magazine.