Between GameStop, Silver, Stimulus, and COVID-19 Progress, it’s fair to say that 2021 is keeping things interesting! If you have been following how this impacts the real estate market, then you will know that the latest headlines have all been pointing at an increase in interest rates. I wanted to break this down for you because we are still in unprecedented economic times, and it’s important that if interest rates do increase, you know how it will impact a buyer’s purchasing power.

First and foremost, I want to state that I do not personally believe that interest rates will increase enough to slow demand. There are some economists and journalists stating that rates could go up as high as 4%. This is very unlikely because the Federal Reserve is currently purchasing Mortgage Back Securities (MBS) and have committed to do so until 2023. That being said, they are not the only buyers of mortgage-backed securities… which is why when the whole GameStop fiasco happened, we saw an uptick in rates as hedge funds pulled out of their MBS holdings to cover their “shorts” (all puns intended).

There is also concern that 1.9 Trillion dollar stimulus will bring about higher interest rates. This is because as the government borrows funds, it creates more treasury bonds. More supply in bonds means that their value drops, and less investors are interested in purchasing them. Since bonds and Mortgage-backed securities are similarly traded, many people believe that what happens to bonds will also happen to the MBS market. However, I want to remind you they only trade closely because they are similar type investments… long term, lower return, typically very secure,: and have minimal credit risks. Make no mistake- They do NOT have a direct correlation to one another. How the bond market reacts to stimulus does not have a direct impact on mortgage-backed securities. What happens to the MBS market is a result of investors’ interest in higher producing investments like the stock market.

Well, that was my two cents! Here is what the experts are saying… literally:

Housing Wire-

– Housing Data Analyst- “ Once we get a vaccine distributed and better treatments, that last 10 million Americans who are still unemployed should be able to find work. That income, plus the fiscal aid and monetary aid should drive up inflation just a little bit higher and the demand should be higher and growth should be back to normal… Slow and steady growth of the US economy will be a driver of higher mortgage rates next year”. *To summarize, he believes rates will increase in 2021 but should not surpass 4% He believes that mortgage rates will follow the state of the economy- meaning the healthier the economy the higher the rates.

National Association of Realtors- Lawrence Yun- Chief Economist “ …in 2021, I think rates will be similar or modestly higher, maybe 3%. So mortgage rates will continue to be historically favorable.” “The Federal Reserve has indicated they want to pursue this low-interest rate policy for a long period, over the next two or three years…” *Short and sweet… Yun believes that rates will remain stable in 2021 due to the actions taken by the Federal Reserve.

– @DaniellehaleDanielle Hale — Chief Economist- Making any kind of prediction for next year is difficult. But our expectation is that mortgage rates start the year roughly in line with where they are now, and they stay fairly low — right around 3% — for the first half of the year,” … “Mortgage rates could approach 3.4% by the end of the year”. *This was one of the more rate aggressive predictions. She believes, like Mohtashami, that as we see the economy improves, rates will increase and the demand for housing will slow down.

Freddie Mac- Len Kiefer- Deputy Chief Economist- “Our forecast is that rates will be relatively flat next year. They might bounce around a little bit, maybe modestly higher at the end of next year, but pretty flat over the next 12 months. The key thing for the early part of 2021 is going to be what happens with the pandemic, If the economy opens up, we may see interest rates start to rise a little bit.” *Personally I think that Freddie Mac data is some of the most accurate out there. Kiefer’s predictions are similar to the other economists in that they believe that interest rates are tied to economic recovery. He and Yun are both optimistic that rates will remain low as a result of the Fed actions with Mortgage-Backed Securities.

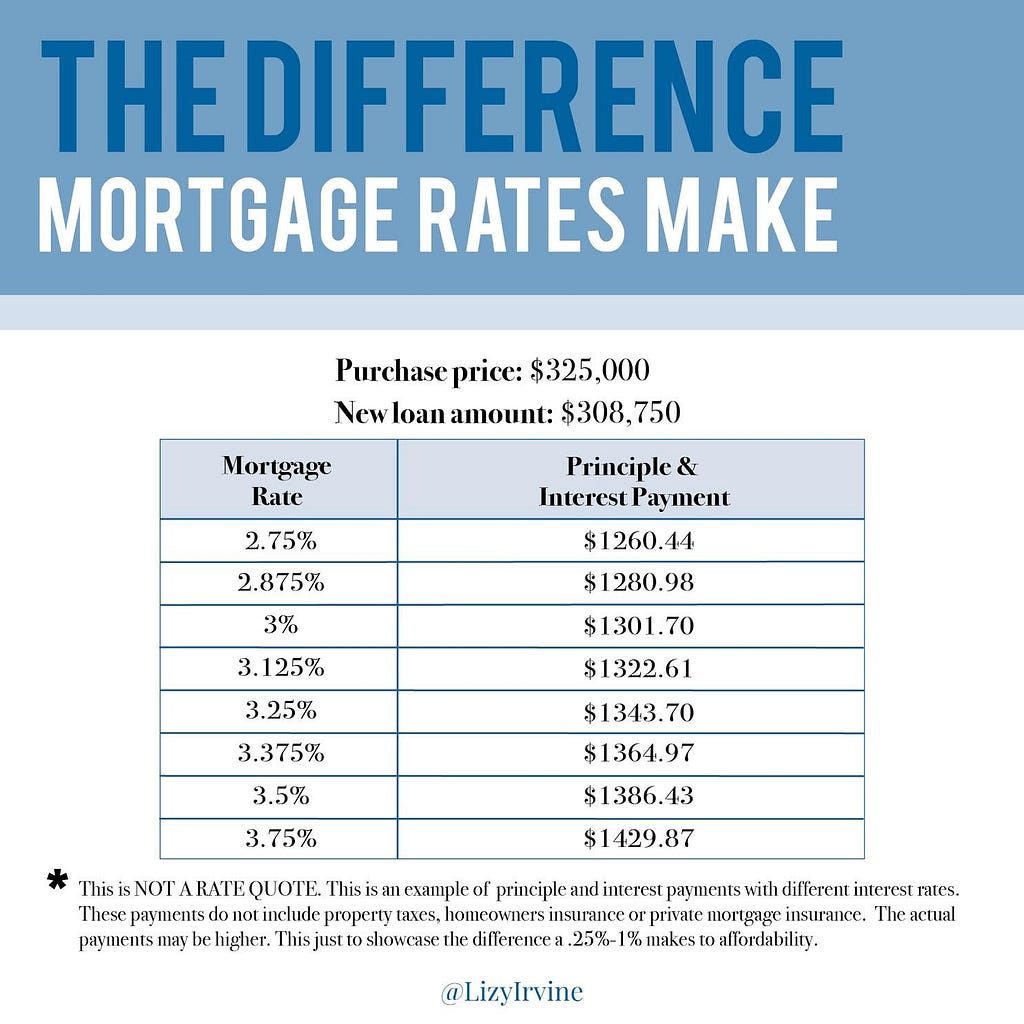

So, what does it look like for buyers in this market? I came up with the following chart to show you as an example (let me repeat… example, because this is NOT a rate quote) of what happens to a payment with an increase of 1%. For this example, I used a purchase price of $325,000 with a 5% down payment (because that was the median sale price in 2020, and the majority of home buyers are using low down conventional and FHA products.

My hope is that this points out how interest rates have more of an impact on affordability than the price of homes. If you are on the fence or have a client that is on the fence, there has never been a more affordable time to buy or refinance. If you or someone you know is waiting for interest rates to drop again or for the market to bottom out, you could be waiting for never.

As always, I am happy to answer any questions you have, and my team is always here to review your mortgage scenarios!

Don’t forget to watch my latest YouTube video and follow @Lizyirvine on Instagram for more helpful mortgage and market information.

Resources:

Mortgage Rates Will Rise in 2021, According to 5 Experts. Here’s What That Means for You

Getty Images It’s been a wild year for the mortgage industry, with rates hitting record lows numerous times. But if you…

Disclaimer: This is NOT A RATE QUOTE. This is an example of principle and interest payments with different interest rates. These payments do not include property taxes, homeowners insurance, or private mortgage insurance. Actual payments may be higher. This just to showcase the difference a .25%-1% makes to affordability. If you have any questions during your research, do not hesitate to give my team of mortgage professionals a call!

Check out our new platform 👉 https://thecapital.io/

https://twitter.com/thecapital_io

What’s Next for Interest Rates was originally published in The Capital on Medium, where people are continuing the conversation by highlighting and responding to this story.